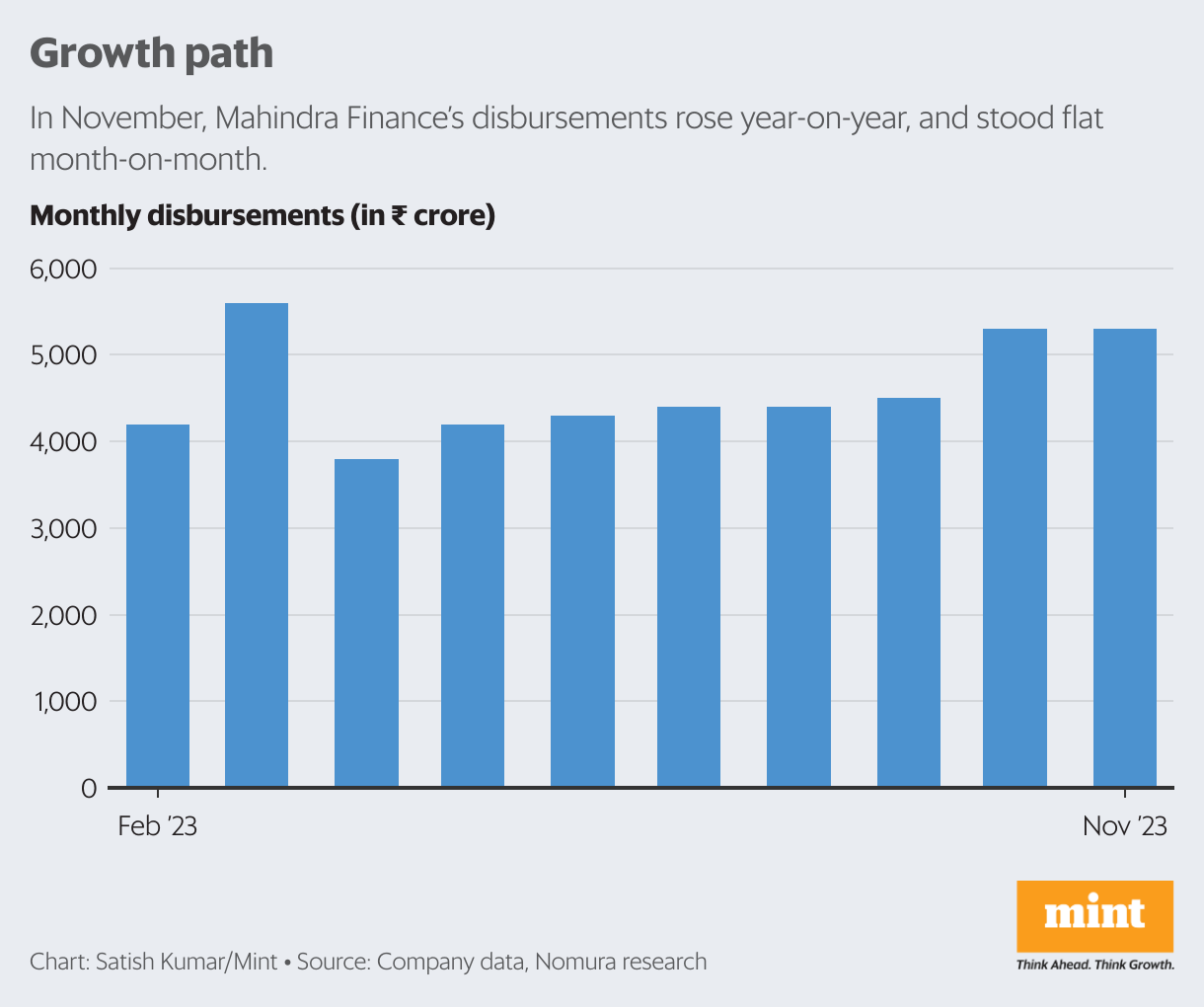

Shares of Mahindra & Mahindra Financial Services Ltd (Mahindra Finance) have fallen by 1.6% since it reported its November growth numbers last week, while the Nifty 50 index has risen 1.3%. The non-banking financial company saw fresh loan disbursements of ₹5,300 crore in November, which is flat month-on-month.

Year-on-year growth stood at about 16%, which is in line with the growth seen so far this year. Total assets under management (AUM), also referred to as gross business assets, stood at ₹96,600 crore as of November, up 26% year-on-year.

However, monthly collection efficiency was lower, dropping to 94% from 96% in November 2022. It’s worth mentioning here that Diwali was in November this year and in October in 2022. “This explains the strong year-on-year growth in disbursements and the slight decline in collection efficiency,” said Motilal Oswal Financial Services.

The festive period traditionally sees an uptick in automobile, commercial vehicles and tractor demand, a key asset class for the company’s lending business. This is also the reason the company is likely to report relatively strong December quarter (Q3FY24) numbers.

Note that the automobile lending business including auto/utility vehicles, tractors, cars, commercial vehicles accounted for 95% of Mahindra Finance’s total disbursement in the half year ending September (H1FY24).

For investors, it has been a roller coaster ride this year. After touching a 52-week high of ₹346.55 in July, Mahindra Finance’s shares have slumped by 21% to ₹273.25.

A key disappointment was the company’s Q2 results, in which growth and profitability missed market estimates. Net profit fell by as much as 48% year-on-year to ₹235 crore. Net interest margin (NIM) dropped by 30 basis points sequentially in Q2 to 6.5%. One basis point is one-hundredth of a percentage point. The more-than-expected NIM drop was led by a change in portfolio mix, a rise in cost of funds and lower yields.

Mahindra Finance’s asset quality, largely depicted by the gross stage-3 loans, has improved consistently from Q2FY22 to Q1FY24. Gross stage-3 loans as a percentage of total loans have fallen sharply from double-digits to 4.3% in Q2FY24. While this is a good sign, it should be noted that the metric has remained flat sequentially. Mahindra Finance aspires for it to drop to 3-3.5%.

For FY24, the company aims to deliver 20% growth in AUM. The credit cost guidance for FY24 stands at 1.5-1.7%. This looks difficult to achieve until high provisions are reversed, according to analysts from Nomura Financial Advisory and Securities (India). “Credit cost was 2.6% in H1FY24, and it needs to be about 0.75% in H2FY24 to achieve 1.7% credit cost in FY24,” Nomura’s analysts wrote in a report on 5 December.

As such, investors are likely to track how the festive season has panned out for Mahindra Finance, and look for signs of better rural demand in H2FY24. Further, the company has outlined an aggressive growth plan under its Mission 2025 strategy. Under this, the company aims to double its AUM (versus FY22), increase NIM to 7.5%, and achieve a return on asset of 2.5%.

Meanwhile, the stock has gained 14% in the past year. Many analysts remain cautious on the outlook. Nomura has a ‘reduce’ rating on the stock. Factors that are driving its rating include: underwhelming profitability on a structural basis with 5/10-year return on equity being 9%/11%, the lowest among its peers; and expensive valuation given growth/profitability profile of the company. Hereon, investors will watch out for improving credit cost and better NIM.

{kind=link}